Barclays & Citi Global Offers – Established Multinational Strength in 2026

When applying for a credit card, one of the most common questions isn’t just about approval — it’s about timing.

How fast will I get a response?

In 2026, response speed has become a competitive advantage. Many global and digital institutions are refining automated decision systems, allowing applications to be processed in significantly shorter windows.

While no issuer guarantees approval within a specific timeframe, certain types of credit cards are more likely to provide responses within 24–48 hours under the right conditions.

Understanding which segments move faster can help you align urgency with strategy.

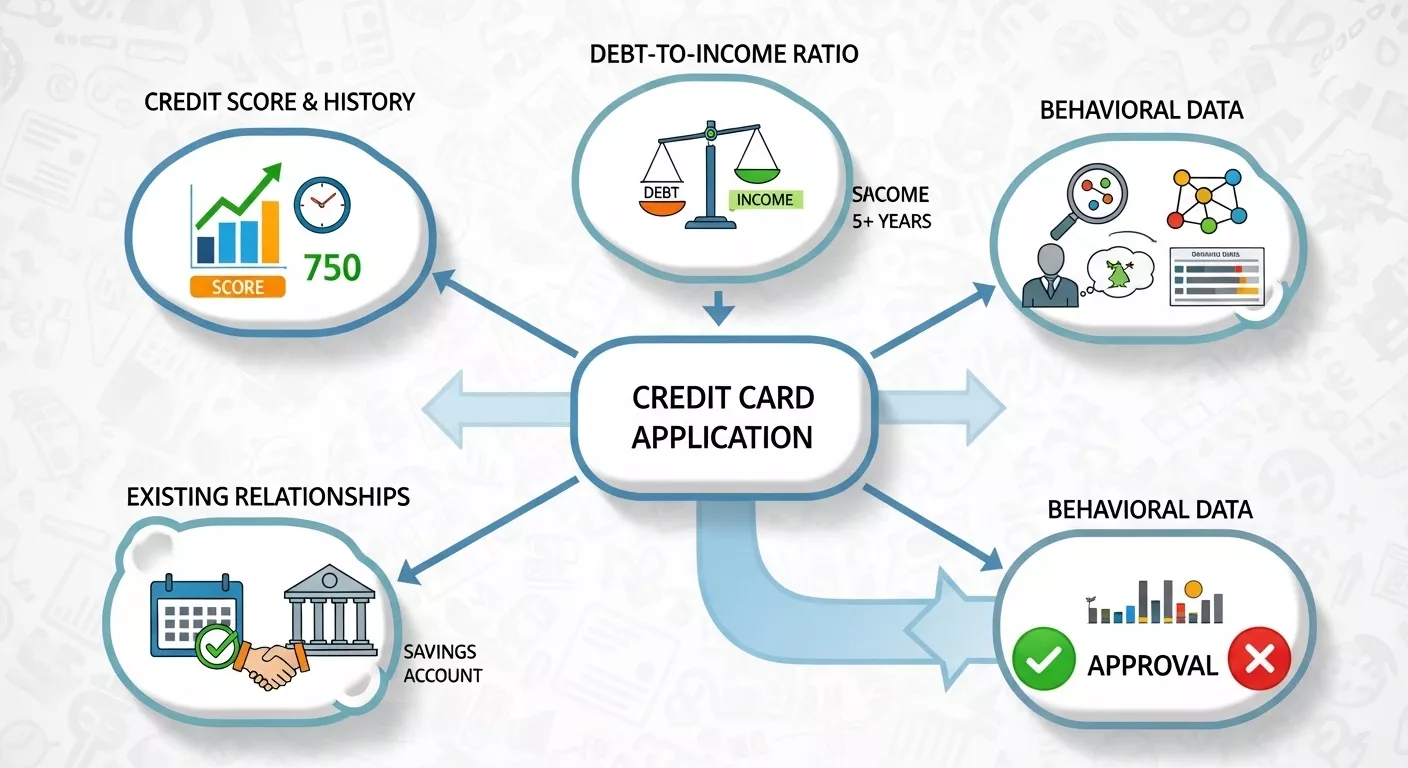

Digital transformation has reshaped credit evaluation.

Banks now rely on:

• Automated risk engines

• Real-time data verification

• Instant identity confirmation

• Integrated credit bureau analysis

• AI-based behavioral scoring

Digital-first institutions often operate with faster internal pipelines, reducing manual review time.

Traditional global banks have also invested heavily in onboarding infrastructure to remain competitive.

As a result, response cycles that previously took several days may now happen within hours in certain segments.

Speed, however, depends on profile clarity and system confidence.

While response time varies by applicant profile, the following categories are more likely to deliver quicker decisions:

Fintech platforms such as:

• Revolut

• Wise

• Monzo

• N26

…typically operate with automated evaluation systems.

These institutions prioritize:

• Fast onboarding

• App-based verification

• Streamlined document review

For applicants with stable and clean profiles, digital products often produce quicker responses.

Mid-tier cashback products from institutions like:

• Capital One

• Citi

• Barclays

…often operate within more competitive onboarding environments.

When promotional cycles are active, response speed may increase as part of customer acquisition momentum.

However, internal sensitivity still applies.

Applicants with existing relationships at institutions such as:

• American Express

• HSBC

• Chase

…may experience smoother and faster internal routing if their profile data is already integrated within the bank’s ecosystem.

Relationship depth can reduce friction.

Even fast-response cards may take longer if the system flags uncertainty.

Common delay triggers include:

• Multiple recent credit inquiries

• Identity verification mismatches

• Elevated utilization

• Inconsistent income documentation

• Cross-institution exposure spikes

Automated systems prioritize clarity.

When signals conflict, manual review may extend timelines.

Response speed can also be influenced by broader market cycles.

Faster windows often coincide with:

• Competitive promotional phases

• Expansion cycles in digital platforms

• Increased customer acquisition campaigns

• Stable macroeconomic signals

Monitoring broader approval trends provides context.

Speed is not random.

It often reflects competitive positioning.

Choosing a fast-response card depends on your objective.

Consider prioritizing speed if:

• You need quick purchasing capacity

• You are testing approval positioning

• You prefer digital onboarding simplicity

• You want rapid decision clarity

However, speed should align with strategy.

High-limit premium products may not always be the fastest segment.

Cashback and digital products often lead in responsiveness.

Alignment matters more than urgency alone.

Cards that appear highly responsive this week may adjust next month.

Digital onboarding evolves.

Internal thresholds recalibrate.

Competitive momentum shifts.

If speed is your priority, reviewing current positioning before applying increases clarity.

Observing movement first reduces uncertainty.

If fast response is important to you, the next step is to review which credit cards are currently positioned strongly in today’s approval environment.

Instead of guessing, evaluate options showing competitive onboarding momentum.

{kind=link}