Barclays & Citi Global Offers – Established Multinational Strength in 2026

The credit card approval environment in 2026 is more fluid than it has been in recent years. While most applicants focus on visible features such as cashback percentages or annual fees, approval behavior itself is quietly evolving behind the scenes. Internal scoring systems, portfolio risk adjustments, and competitive positioning strategies are constantly being refined by global banks and digital institutions.

What looks like a stable approval process from the outside often operates under dynamic internal thresholds. Small shifts in evaluation sensitivity, onboarding speed, or promotional emphasis can significantly influence how applications are processed.

Understanding these trends before applying allows you to approach the process with more strategic awareness.

One of the most noticeable developments in 2026 is the increase in dynamic filtering. Instead of relying on fixed approval criteria, many institutions now adjust internal thresholds more frequently based on:

• Application volume

• Portfolio exposure

• Macroeconomic signals

• Regional demand

• Behavioral data patterns

When application activity rises sharply, internal systems may temporarily tighten. When banks seek expansion, filters may become more flexible. These shifts are rarely announced publicly, yet they influence approval timing.

Digital-first banks, in particular, have adopted adaptive underwriting models that respond more quickly to changing conditions. This creates shorter cycles of flexibility and sensitivity throughout the year.

Another major trend is the acceleration of decision timelines, especially among global fintech platforms and digitally native institutions.

Banks such as Revolut, Wise, Monzo, and N26 continue refining automated onboarding systems. Traditional global players like American Express, HSBC, Citi, and Capital One are also investing heavily in digital infrastructure.

As a result, many applicants are experiencing:

• Faster pre-approval signals

• Shorter response windows

• More streamlined identity verification

• Increased use of automated risk modeling

This does not necessarily mean approvals are easier. It means decisions are becoming faster and more data-driven.

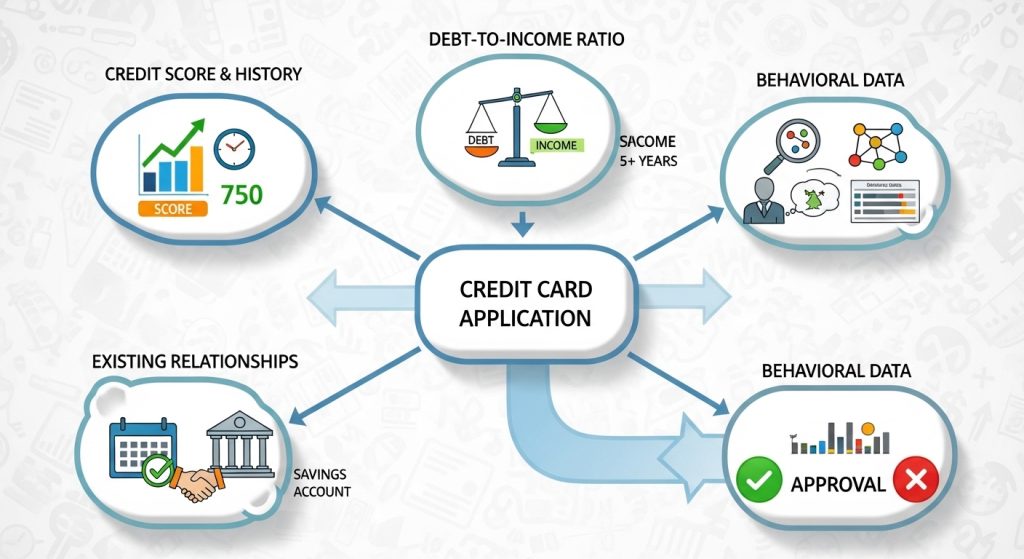

In 2026, behavioral stability appears to be receiving greater attention than isolated financial metrics. While income and credit score remain important, internal evaluation systems increasingly analyze patterns such as:

• Recent inquiry frequency

• Credit utilization trends

• Account longevity

• Payment behavior consistency

• Overall exposure across institutions

Rather than focusing solely on income thresholds, many banks are emphasizing long-term profile reliability. Applicants who demonstrate steady financial behavior may benefit from more predictable outcomes.

This shift suggests that timing and profile positioning matter more than ever.

The cashback category continues to attract significant competition in 2026. Global banks and digital platforms are actively refining reward structures to remain competitive. This results in:

• Higher visible cashback percentages in certain segments

• Temporary promotional boosts

• Rotating bonus categories

• Short-term sign-up incentives

However, increased competition does not always translate into relaxed approval sensitivity. In some cases, higher promotional intensity is accompanied by more selective internal screening.

Understanding that promotional generosity and approval flexibility are not always aligned is essential.

While mid-tier products remain competitive, certain premium credit cards offering higher limits appear to operate under more selective internal standards during specific periods.

Premium-tier shifts may include:

• Higher sensitivity to recent inquiries

• Greater scrutiny of credit exposure

• More emphasis on income stability

• Increased attention to utilization ratios

These refinements do not necessarily signal reduced opportunity. Instead, they highlight the importance of profile positioning before applying for higher-limit products.

Because many major institutions operate internationally, approval trends are increasingly influenced by broader economic and regulatory conditions. Global players such as Barclays, HSBC, Citi, Chase, and American Express adjust internal strategies based on cross-regional portfolio data.

This interconnectedness means that trends observed in one region may reflect broader portfolio management strategies rather than isolated local factors.

For English-speaking applicants worldwide, monitoring global patterns provides useful context.

The key takeaway is not that approval has become harder or easier in 2026. It is that approval behavior has become more adaptive.

Instead of assuming fixed criteria, applicants should consider:

• Is this a period of expansion or caution?

• Are digital banks accelerating onboarding?

• Are promotional campaigns aligned with approval flexibility?

• Is my profile stable relative to current trends?

Observing market movement first reduces uncertainty.

Applying without context increases unpredictability.

Most comparison pages focus exclusively on product features. Very few address how approval behavior evolves over time.

By reviewing current trends before evaluating specific offers, you position yourself more strategically. This reduces reactive decision-making and increases clarity.

Approval systems are data-driven and dynamic.

Your approach should be informed and intentional.

Now that you understand how approval behavior is shifting in 2026, the next logical step is to examine how banks evaluate applications internally.

Understanding evaluation criteria helps you align timing, positioning, and strategy before choosing a specific card.